Select a region

Policy & Resources will urge deputies to again back its defeated tax and social security package on top of hundreds of millions worth of borrowing to ensure all infrastructure projects can proceed in a sustainable way.

It estimates that the islands’ cash reserves will be more than wiped out within seven years if the States proceed with the hospital modernisation and rebuild of Les Ozouets campus for education without finding new ways of paying the bills.

Deputy Mark Helyar, Committee Vice President and treasury lead, said this includes both the existing capital reserve, some £500m, and remaining cash from the bond vanishing within years if there is no change to revenue raising or appetite for major projects at a media briefing this afternoon.

He warned of the danger of a “double whammy” over having no money in the pot and the loss of investment returns from that pot. “We really must urgently do something to correct this position. This is not a long way away… this is something that will happen imminently.”

The key message from the briefing was to ensure the island has enough money cashed away throughout the coming decades to pay for the future.

The best way to do this, while spending on new and necessary infrastructure through borrowing, is to fund it through a fair and progressive tax system, Deputy Peter Ferbrache said.

“The States must now agree what it wants and how to pay for it… it’s make up your mind time.”

He added that P&R would lead on it and seek to win more hearts and minds among politicians and the public than it has been able to so far.

P&R still estimates that the implementation of tax reform will take two years, meaning changes would be implemented in October 2025 at the earliest - just months after the next States takes office.

The newly appointed panel of independent fiscal experts will scrutinise and publish comment on the data prior to the States debate in October.

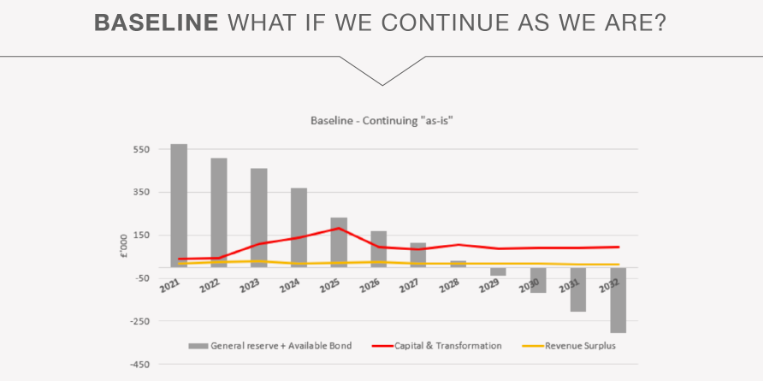

Pictured: P&R forecasts that the island will quickly move into a negative financial position if nothing changes.

P&R will present the following options to deputies in the October States debate, but it has identified “core” spending which it thinks must make the cut no matter what deputies decide.

This includes raising £25m per year from new corporate taxes, and transport taxes. Identifying and delivering savings and efficiencies in the public sector worth £10m per year. £3m per year for “essential” policy development, and the execution of 17 major building projects which are at an advanced stage for £95m.

Option 1: Borrow nothing, but possibly use the remnants of the bond worth £160m. Spend up to £95m on other capital projects including purchasing housing and developing infrastructure on the Bridge and health and community services. Stop all other major projects such as the hospital modernisation, post-16 campus and inert waste.

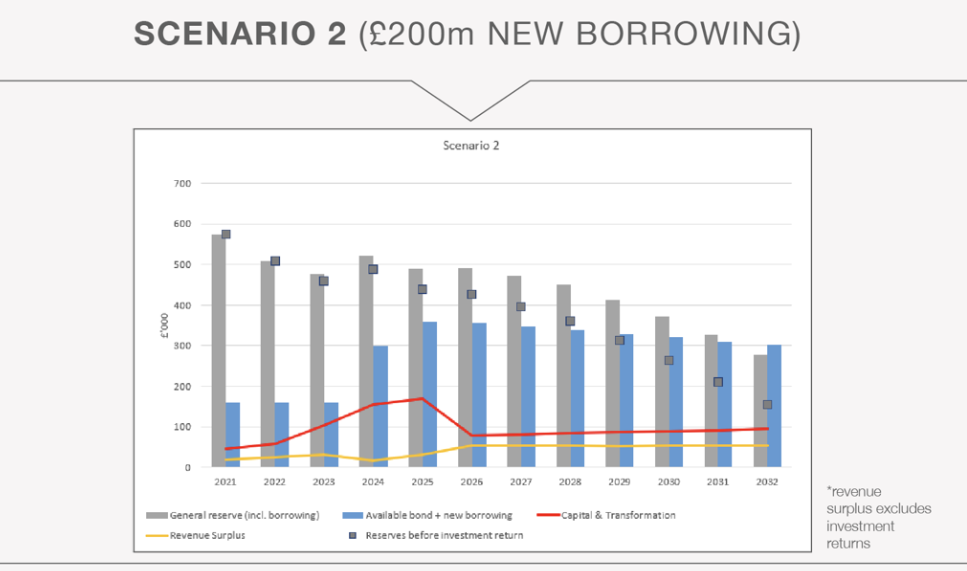

Option 2: Borrow £200m and release cash from the health service reserve, currently totalling £3.5m, to help fund the hospital project as part of increased capital project spending of up to £345m, which would also include the Les Ozouets redevelopment.

Option 3 (P&R’s preferred option): Borrow £350m to help fund all agreed capital projects worth up to £425m and £2.5m worth of social and community initiatives, repaying the debt through a reformed tax and social security system. That will include elements common in the Committees’ defeated tax package; a broad-based goods and services tax, a lower band of income tax for earnings up to £30,000 per year, a raised personal income tax allowance, personal allowances for social security contributions, and inflation-mitigating increases to States benefits.

P&R advised these options are subject to change upon final publication of the proposals on 11 September, and for any amendments which other deputies may table as debate draws nearer.

Pictured: Option 2 is evidenced to also be unsustainable in the long-term.

The senior politicians argued that while the second option may appear the most tempting, it could be the most destructive in the long-term with spending projected to outstrip cash levels in reserve by 2032.

Deputy Jonathan Le Tocq warned of “massive risks” of using the health reserve for anything other than its intended purposes.

But he also said that putting off spending on capital projects in Option 1 “will be worse for future generations” while slowly dwindling reserves may make it more difficult to borrow in future.

Option 3 may represent huge levels of borrowing for several years but it would be serviced by “sustainable” tax rises which would see reserves dip in the middle of the decade as projects are delivered but grow and remain high before investment returns well into the 2030s, he added.

Deputy Bob Murray said that plan was “only just sustainable” but was better than the alternatives in the long-term.

The island is in a “good position to borrow” which would prevent the drying up of “limited cash reserves”, he added. He admitted this was “not the Guernsey way”, however, and even though interest rates are high and will stay so “raging” inflation has rendered many agreed projects unaffordable.

There were echoes of uncertainty over what may happen should the government, which comprises the entire chamber of deputies, fail to reach a conclusion, or what P&R would do if it again cannot find support.

“We will see what happens… we will see what state we are in,” Deputy Ferbrache said.

Deputy Le Tocq indicated that he has given up trying to convince others who believe “these tens and tens of millions are there” but said it wouldn’t be impossible to find extra votes.

Committee members called on other politicians to “do what is right” in the interests of the island.

“Successive States have not grasped the nettle,” Deputy David Mahoney said, suggesting that underspending on critical infrastructure will “come home to roost” in the same way that underspending on house repairs does.

Meanwhile he sought to dispel the “same old trope that problems will be solved by cutting staff and cutting costs”.

The Committee will nevertheless report back at the end of this year with suggestions for how to drive tens of millions of pounds worth of savings per year in the public sector, he added, with those anticipated savings baked into the financial modelling.

Comments

Comments on this story express the views of the commentator only, not Bailiwick Publishing. We are unable to guarantee the accuracy of any of those comments.